Beranda

/ Insurance Expense Adjusting Entry / Adjusting Entries Prezentaciya Onlajn - The repairs expense is a debit entry usually and we will debit it in a later journal, but here it is a credit.

Insurance Expense Adjusting Entry / Adjusting Entries Prezentaciya Onlajn - The repairs expense is a debit entry usually and we will debit it in a later journal, but here it is a credit.

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

Insurance Expense Adjusting Entry / Adjusting Entries Prezentaciya Onlajn - The repairs expense is a debit entry usually and we will debit it in a later journal, but here it is a credit.. The balance in insurance expense starts with a zero balance each year and increases during the year as the account is. Adjusting entries are required to record internal transactions and to bring assets and liability accounts to their proper balances and record expenses or revenues in the proper accounting period. Continue to perform your adjusting entries. Likewise, the company can make insurance expense journal entry by debiting insurance expense account and crediting prepaid insurance account. On december 31, an adjusting journal entry is made because it is the end of an accounting period and microtrain has not used all of the insurance they paid for.

After making the entry, the balance of the unused service supplies is now at $600 ($1,500 debit and $900 credit). Insurance expense journal entry an insurance expense occurs after a small business signs up with an insurance provider to receive protection cover. Any prepaid expense should be recorded similarly. Adjusting entries can also be prepared monthly, especially if the company needs updated monthly account balances. Service supplies expense now has a balance of $900.

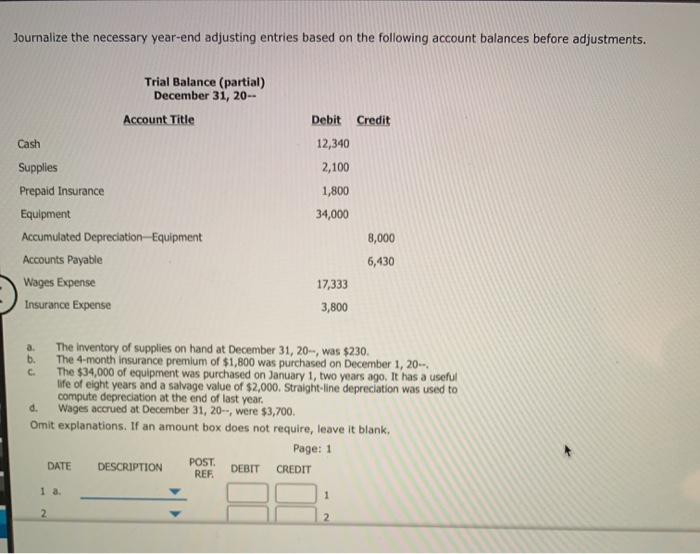

Journalize The Necessary Year End Adjusting Entries Chegg Com from media.cheggcdn.com Expenses paid in cash before use or consumption. Microtrain will record an adjusting entry for 1 month of insurance expense ($2,400 / 12 months) since the policy began december 1 and the year end is december 31. The entire premium may also be recorded initially as insurance expense. Adjusting entries are required at the end of each fiscal period to align the revenues and expenses to the right period, in accord with the matching principle Likewise, the company can make insurance expense journal entry by debiting insurance expense account and crediting prepaid insurance account. The repairs expense is a debit entry usually and we will debit it in a later journal, but here it is a credit. Continue to perform your adjusting entries. The best example with which you are all familiar is the recorded expense adjusting entry for depreciation, amortization, and depletion.

The cost has been recorded as assets or liabilities and but will be recognized as expenses or liabilities over time or through the normal operations of the business.

In order to create accurate financial statements, you must create adjusting entries for your expense, revenue, and depreciation accounts. Adjusting entry for annual depreciation expense for equipment. To recognize prepaid expenses that become actual expenses, use adjusting entries. What adjusting entry is necessary at december 31, the end of the accounting year? Adjusting entries are most commonly used in accordance with the matching principle to match revenue and expenses in the. Adjusting entries are made at the end of an accounting. Microtrain will record an adjusting entry for 1 month of insurance expense ($2,400 / 12 months) since the policy began december 1 and the year end is december 31. An increase (debit) to an expense account and a decrease (credit) to an asset account. It is assumed that the decrease in the amount prepaid was the amount being used or expiring during the current accounting period. After making the entry, the balance of the unused service supplies is now at $600 ($1,500 debit and $900 credit). Deduct your new expense from your current asset balance. Adjusting entries, also called adjusting journal entries, are journal entries made at the end of a period to correct accounts before the financial statements are prepared. Adjusting entry for repair services received that was originally paid as cash in advance to the supplier in the previous month.

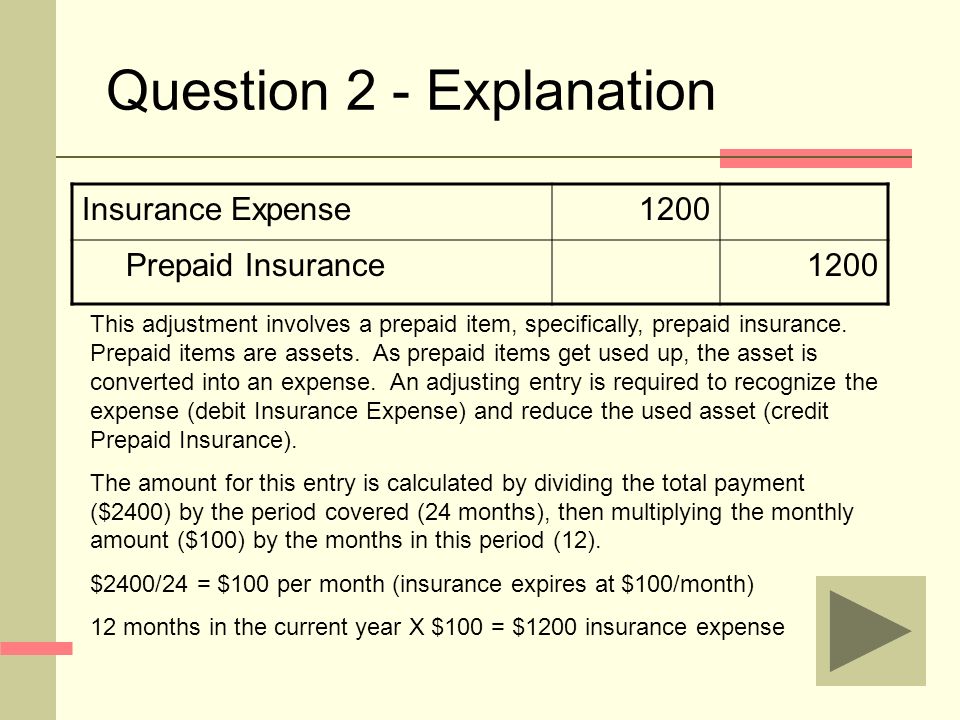

It is assumed that the decrease in the amount prepaid was the amount being used or expiring during the current accounting period. As you use the prepaid item, decrease your prepaid expense account and increase your actual expense account. Microtrain will record an adjusting entry for 1 month of insurance expense ($2,400 / 12 months) since the policy began december 1 and the year end is december 31. Likewise, the company can make insurance expense journal entry by debiting insurance expense account and crediting prepaid insurance account. Adjusting entries are made at the end of an accounting.

Principles Of Accounting I Acct 1104 Adjusting Entries Review Click Here To Proceed Ppt Download from images.slideplayer.com This video explains the income statement method for adjusting entries for prepaid insurance / insurance expense.note that the end result, on the financial st. Adjusting entries are most commonly used in accordance with the matching principle to match revenue and expenses in the. The service supplies expense is an expense account while service supplies is an asset. Adjusting entries, also called adjusting journal entries, are journal entries made at the end of a period to correct accounts before the financial statements are prepared. The insurance provider charges an annual fee, called a premium, which will cover the business for 12 months. An increase (debit) to an expense account and a decrease (credit) to an asset account. As a result of the above entry and adjusting entry, the income statement for 20x1 would report insurance expense of $3,000, and the balance sheet at the end of 20x1 would report prepaid insurance of $6,000 ($9,000 debit less $3,000 credit). Insurance expires at the rate of $200 per month.

What adjusting entry is necessary at december 31, the end of the accounting year?

Therefore adjusting entries always affect one income statement account (revenue or expense) and one balance sheet account (asset or liability). The adjusting entry would be: The balance in insurance expense starts with a zero balance each year and increases during the year as the account is. Adjusting entries can also be prepared monthly, especially if the company needs updated monthly account balances. The repairs expense is a debit entry usually and we will debit it in a later journal, but here it is a credit. Depreciation expense, insurance expense, interest payable, and supplies expense. This is the fourth step in the accounting cycle. Any prepaid expense should be recorded similarly. The service supplies expense is an expense account while service supplies is an asset. In order to create accurate financial statements, you must create adjusting entries for your expense, revenue, and depreciation accounts. On december 31, an adjusting journal entry is made because it is the end of an accounting period and microtrain has not used all of the insurance they paid for. The adjusting entry would be: Prepare the adjusting entries at march 31, assuming that adjusting entries are made quarterly.

The best example with which you are all familiar is the recorded expense adjusting entry for depreciation, amortization, and depletion. Adjusting entries are required at the end of each fiscal period to align the revenues and expenses to the right period, in accord with the matching principle The cost has been recorded as assets or liabilities and but will be recognized as expenses or liabilities over time or through the normal operations of the business. On december 31 2016 the expired portion of prepaid insurance 1800 312 450 will be converted into expense by making the following adjusting entry. In the adjustment is for section, select company adjustment.

Answered 1 Journalize The Adjusting Entries Bartleby from prod-qna-question-images.s3.amazonaws.com As you use the prepaid item, decrease your prepaid expense account and increase your actual expense account. The income statement account insurance expense has been increased by the $900 adjusting entry. As a result of the above entry and adjusting entry, the income statement for 20x1 would report insurance expense of $3,000, and the balance sheet at the end of 20x1 would report prepaid insurance of $6,000 ($9,000 debit less $3,000 credit). This is the fourth step in the accounting cycle. To recognize prepaid expenses that become actual expenses, use adjusting entries. Prepare the adjusting entries at march 31, assuming that adjusting entries are made quarterly. Service supplies expense now has a balance of $900. At the end of the year, prepaid insurance would have a balance of $2,250 and insurance expense would be at $750.

Dr cash/bank ($14,000 x 0.75) $10,500 cr insurer (debtor) $10,500 insurer pays out the 75%.

The best example with which you are all familiar is the recorded expense adjusting entry for depreciation, amortization, and depletion. After making the entry, the balance of the unused service supplies is now at $600 ($1,500 debit and $900 credit). Dr cash/bank ($14,000 x 0.75) $10,500 cr insurer (debtor) $10,500 insurer pays out the 75%. Click the item name column and choose the correct health insurance payroll item. It is assumed that the decrease in the amount prepaid was the amount being used or expiring during the current accounting period. Adjusting entries can also be prepared monthly, especially if the company needs updated monthly account balances. Adjusting entries are made at the end of an accounting. Likewise, the company can make insurance expense journal entry by debiting insurance expense account and crediting prepaid insurance account. An adjusting entry is made at the end of accounting period for converting an appropriate portion of the asset into expense. Therefore adjusting entries always affect one income statement account (revenue or expense) and one balance sheet account (asset or liability). Each month, an adjusting entry will be made to expense $10,000 (1/12 of the prepaid amount) to the income statement through a credit to prepaid insurance and a debit to insurance expense. Prepare the adjusting entries at march 31, assuming that adjusting entries are made quarterly. This is the fourth step in the accounting cycle.